A booster club investment policy is the written framework that governs how your organization holds, invests, and spends its financial assets — and, critically, which categories of funds carry restrictions that constrain how earnings can flow. For most booster clubs, the policy applies to three distinct fund types: general reserves that must stay accessible for operations, restricted gifts that a sponsor or donor designated for a specific purpose, and recognition funds set aside to support awards, digital hall of fame programs, trophy cases, and other multi-season athletic recognition commitments.

Without a documented investment policy, each treasurer interprets these distinctions differently. That inconsistency can expose the organization to governance problems or, in serious cases, misapplication of restricted funds — often without any officer realizing it until a donor asks where their gift went.

Not legal, financial, or tax advice: This article describes common practices for educational purposes only. Booster club policies and legal requirements vary significantly by state, school district structure, and the organization’s nonprofit classification. Consult a licensed CPA, attorney, or your school district’s finance office before establishing or revising investment policies.

A written booster club investment policy gives the board, treasurer, and incoming officers a shared standard for managing all three fund categories — one that does not depend on any single person’s memory, survives leadership transitions, and satisfies the questions a school administrator or external auditor is most likely to ask.

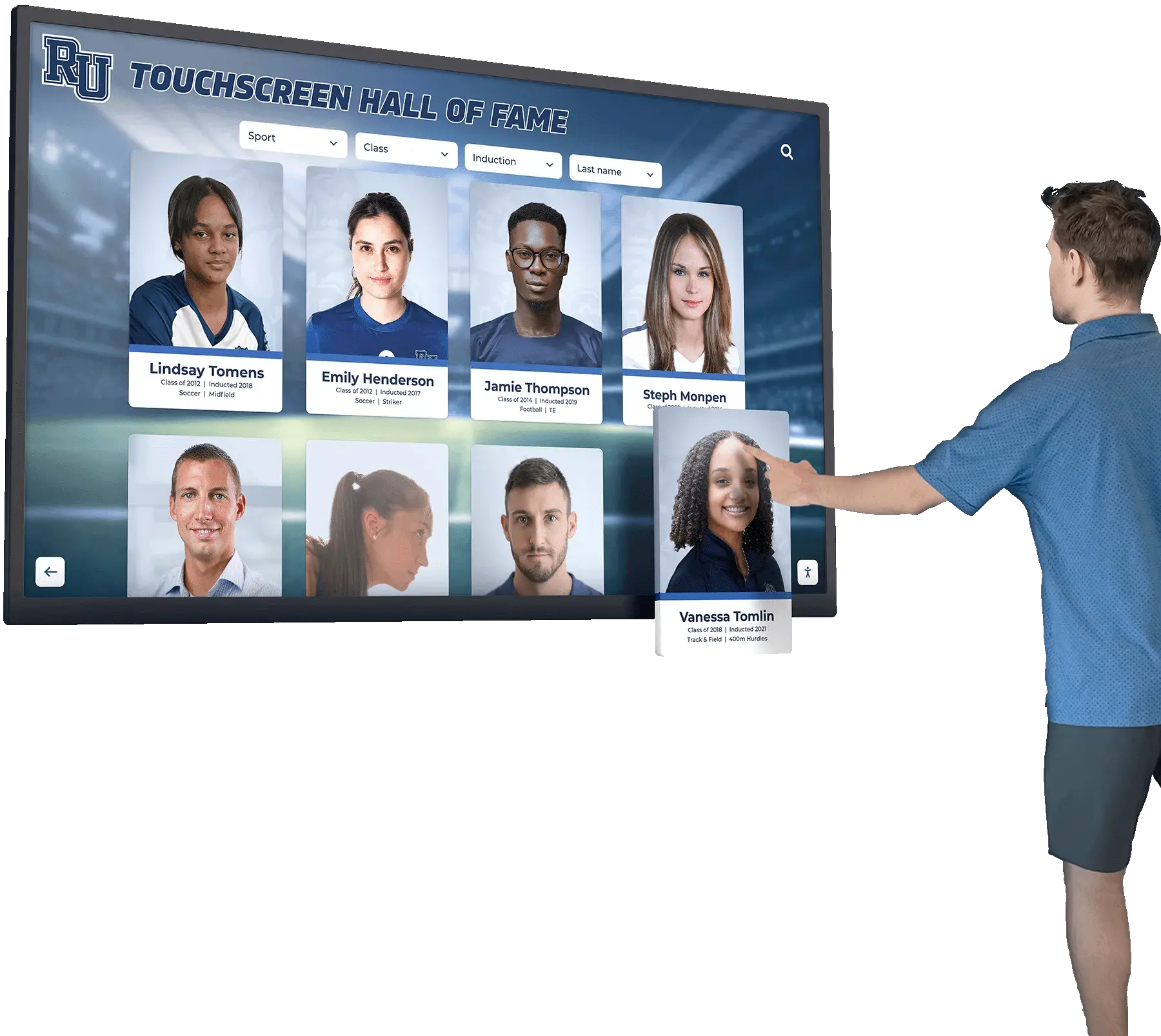

Digital recognition displays represent a multi-season commitment that recognition fund earnings may support — a sound booster club investment policy documents how those funds are invested and how earnings flow to recognition programs

What Is a Booster Club Investment Policy?

A booster club investment policy — formally called an Investment Policy Statement, or IPS — is a board-approved document that defines the rules under which the organization’s financial assets are managed. It specifies what types of assets may be held, what risk levels are acceptable for each fund category, how funds are allocated between liquid reserves and longer-term instruments, and what process is required to deviate from those rules.

For a small booster club whose assets consist entirely of a checking account and a savings account, the policy may be brief. For an organization that manages a substantial reserve, a multi-year restricted gift from a local business, or a dedicated recognition endowment, the policy needs enough specificity to address each fund category independently.

The Investment Policy Statement is not the same as the reserve policy — though the two documents overlap. The reserve policy defines how much the organization holds in reserve and what that reserve is designed to protect. The investment policy governs how every category of financial assets, including the reserve, is held and managed. Programs that have adopted a reserve policy but lack an investment policy have addressed only one half of the governance framework their financial position requires.

According to guidance from the National Council of Nonprofits, a nonprofit organization’s investment policy should at minimum address: investment objectives, risk tolerance, asset allocation, liquidity requirements, prohibited investments, and review schedule. Each of those elements applies directly to booster clubs managing reserves, restricted gifts, and recognition funds.

Core Components of an Investment Policy Statement

Every booster club investment policy, regardless of the organization’s size, should address the following components. The level of detail scales with the complexity of the organization’s financial position.

Investment Objectives

State why funds are being held and what they are expected to accomplish. For a general operating reserve, the objective is liquidity and principal preservation — the funds need to be accessible on short notice and must not lose value. For a recognition fund intended to support an ongoing award program, the objective may be to generate modest earnings over time while preserving the principal that funds the award itself.

Stating the objective in writing allows the board to evaluate whether actual investment decisions align with the stated purpose, and gives incoming officers clear guidance on what each fund is designed to accomplish.

Risk Tolerance by Fund Category

Not all funds carry the same risk tolerance. A reserve that must cover three months of operations cannot be invested in any vehicle with meaningful principal risk, because the organization may need those funds on short notice. A recognition fund that will not be drawn on for several years can absorb more variability in exchange for higher expected returns.

The investment policy should specify risk tolerance separately for each fund category. A practical approach: Reserves carry low risk tolerance (FDIC-insured bank accounts, money market funds); Restricted gifts carry the risk level specified by the donor’s gift agreement or, absent such guidance, low to moderate risk; Recognition funds carry moderate risk tolerance when the draw-down timeline is long-term, and low risk when recognition commitments will be funded in the near term.

Liquidity Requirements

Specify how quickly each fund category must be accessible in cash. General reserves need high liquidity — ideally same-day or next-day access. Restricted gifts that fund a specific project may be held in a designated account with controlled disbursement. Recognition funds supporting an ongoing award program may have a scheduled annual distribution that does not require immediate liquidity.

Defining liquidity requirements in the policy prevents the common error of investing funds in instruments that match the expected timeline on paper but create a hardship when a recognition commitment comes due unexpectedly or earlier than scheduled.

Prohibited Investments

List investment types the board has determined are inappropriate for the organization’s assets. Common prohibitions for booster club-scale organizations include speculative instruments, derivatives, single-stock positions exceeding a defined concentration limit, and any investments with redemption restrictions longer than the fund’s liquidity requirement.

Spending Policy for Interest and Earnings

For recognition funds and restricted gifts that generate interest or dividend income, the policy must specify what happens to those earnings. The spending policy might state that earnings up to a defined percentage of the fund’s value may be distributed annually to support recognition programs, while any excess is retained to grow the fund. This is particularly relevant for organizations managing a named award endowment or a fund established by a major donor or sponsor to support a perpetual recognition commitment.

Digital hall of fame programs for school athletic organizations illustrate why spending policies matter — a program whose hall of fame software subscription is funded by investment earnings from a recognition endowment needs a clear policy on how much of those earnings may be applied to technology costs each year, and what documentation the board must maintain to demonstrate that the spending aligns with the fund’s stated purpose.

Recognition installations funded through designated recognition funds require the investment policy to explicitly authorize what expense categories those fund distributions may cover — from annual induction costs to ongoing digital display subscriptions

Protecting Reserves: What Goes Liquid vs. What Gets Invested

The most common investment policy question for booster club officers is where to draw the line between funds that stay in a checking or savings account and funds that can be placed in a higher-yielding instrument with some illiquidity.

A practical framework:

Keep liquid (checking, savings, or FDIC-insured money market): Operating reserves covering three to six months of program expenses; any funds pledged to recognition commitments within the next 12 months; restricted gift balances for projects expected to proceed within the year; any funds the board cannot afford to have inaccessible for even a short period.

May invest with modest illiquidity (short-term CDs, Treasury bills, short-duration bond funds): Recognition fund balances not needed within 12 to 24 months; surplus reserves above the ceiling defined in the reserve policy; restricted gift balances for projects with a timeline extending beyond the current season; any funds the board has specifically designated for long-term program investment.

The investment policy should express these guidelines as specific rules — not general principles — so the treasurer can apply them consistently without board deliberation every time a CD matures or a surplus arises.

Digital tools for preserving athletic history and recognition programs show how multi-year recognition commitments create predictable drawdown schedules that directly inform where funds should sit on the liquidity spectrum — an annual software renewal or a biennial display refresh requires a different liquidity structure than a one-time installation payment.

Restricted Gifts: Handling Donor Designations Within the Policy

A restricted gift is any contribution a donor or sponsor has given with a condition on how the funds may be used. Common restrictions for booster clubs include gifts designated for a specific sport, a named award, equipment in a particular facility, or the development of an athletic hall of fame or recognition display.

The investment policy must address restricted funds separately from unrestricted reserves for three reasons:

Commingling risk: Restricted and unrestricted funds that sit in the same account without separate accounting can create legal and governance exposure if the restricted funds are applied to purposes other than those the donor specified. Even when the amounts involved are small, commingling undermines the organization’s ability to demonstrate faithful stewardship if a donor, auditor, or school administrator asks for an accounting.

Earnings attribution: When a restricted gift earns interest, the investment policy must specify whether those earnings remain restricted — subject to the same use conditions as the principal — or flow to the general operating fund. If the gift agreement is silent on this point, the organization’s policy becomes the governing standard.

Return or reversion: If a restricted gift cannot be used for its stated purpose because a program was discontinued, a project was abandoned, or the restriction became impractical, the investment policy should reference the process for seeking donor approval to redirect the funds or, where applicable, the cy pres doctrine under state law.

When a booster club receives a restricted gift for a recognition program — a donation specifically to fund digital recognition technology, to endow a perpetual award, or to install an athletic history display — the investment policy’s restricted fund section governs how those funds are held until they are deployed, how any earnings are treated, and what documentation the board must maintain.

Athletic hall of fame selection and governance processes for school programs frequently involve restricted recognition funds — endowments that support the ongoing operation of induction programs require investment policies that address both principal protection and permissible earnings use, so that the organization can honor multi-decade recognition commitments without revisiting policy basics every year.

Hall of fame installations funded through restricted donor gifts or sponsor designations require the investment policy to address commingling prevention, earnings attribution, and documentation standards that protect both the organization and the donor relationship across leadership transitions

Recognition Funds and How Investment Earnings Support Athletic Commitments

A recognition fund is a category of booster club financial asset specifically set aside to support the organization’s ongoing athletic recognition obligations — award programs, hall of fame operations, digital display technology, trophy case maintenance, and other recognition infrastructure. Unlike general reserves, which protect operating continuity, recognition funds are purpose-driven: they exist to ensure recognition commitments are met independent of fluctuations in annual fundraising revenue.

For organizations with recognition funds large enough to generate meaningful earnings, the investment policy becomes the mechanism through which those earnings support specific recognition commitments. A common structure:

- The fund principal is invested conservatively in short-term instruments with low volatility.

- A defined percentage of the fund’s average balance — often between 4 and 6 percent annually — is distributed to the operating budget for recognition program expenses.

- Earnings above the distribution rate are retained to grow the fund against inflation and expanding recognition obligations.

This structure allows the organization to commit to multi-season recognition programs — including digital display subscriptions, annual award ceremonies, and hall of fame induction costs — with confidence that the funding source is not dependent on any single year’s fundraising cycle.

Digital showcase board systems for school clubs and booster organizations illustrate how technology-forward recognition programs create recurring annual costs — exactly the kind of obligation a recognition fund’s spending distribution is designed to cover without drawing on operating reserves or waiting for each season’s fundraising to close.

What Recognition Costs May the Fund Support?

The investment policy should explicitly list the categories of recognition expense that may be funded from recognition fund distributions. Ambiguity about this creates conflict between officers who interpret “recognition program expenses” broadly and auditors or school administrators who expect a narrower definition.

Permissible categories typically include:

- Annual hall of fame induction costs, including photography, profile production, and physical or digital installation

- Athletic display technology subscriptions, including software licensing, CMS support, and content refresh cycles

- Award materials for sanctioned recognition programs, including plaques, trophies, and certificates

- Ceremony and event costs directly tied to recognition programs

- Photography and archival costs for maintaining the organization’s athletic history record

Categories that typically fall outside recognition fund distributions — and should be funded from operating reserves instead — include general equipment purchases, facility repairs, transportation, and coaching expenses not directly tied to a recognition program.

Interactive student recognition and classroom display programs demonstrate how recognition infrastructure at schools frequently spans both athletic and academic programs — an investment policy with clear category definitions prevents recognition fund distributions from drifting into general program support without board authorization, which protects the fund’s principal and maintains the documentation trail that governance requires.

Investment Policy Decision Table

The following table provides a quick-reference framework for the most common investment policy decisions a booster club board faces. Each row identifies the fund type, its typical investment objective, the appropriate risk level, standard liquidity, and how earnings are treated.

| Fund Type | Investment Objective | Risk Level | Liquidity | Earnings Treatment |

|---|---|---|---|---|

| Operating reserve | Principal preservation, accessibility | Low — FDIC-insured accounts | Same-day to 5 business days | Flows to general operating fund |

| Capital reserve | Preservation plus modest growth | Low to moderate | 30 to 90 days acceptable | Retained in reserve account |

| Restricted gift — near-term project | Preservation until deployment | Low | Must match project timeline | Restricted or general fund per gift agreement |

| Restricted gift — perpetual endowment | Preservation plus inflation hedge | Moderate | Annual distribution only | Defined percentage distributable; balance retained |

| Recognition fund — near-term draws | Preservation, scheduled distributions | Low | Quarterly or semi-annual draws | Distributable per spending policy |

| Recognition fund — long-term endowment | Growth plus scheduled distributions | Moderate | Annual distribution only | 4–6% distribution; balance grows |

| Surplus reserve | Growth until redeployment | Low to moderate | 90 to 180 days acceptable | Retained or transferred per board resolution |

This table does not constitute investment advice. Actual allocations should be approved by the full board and reviewed against the organization’s specific financial position, obligations, and governing documents.

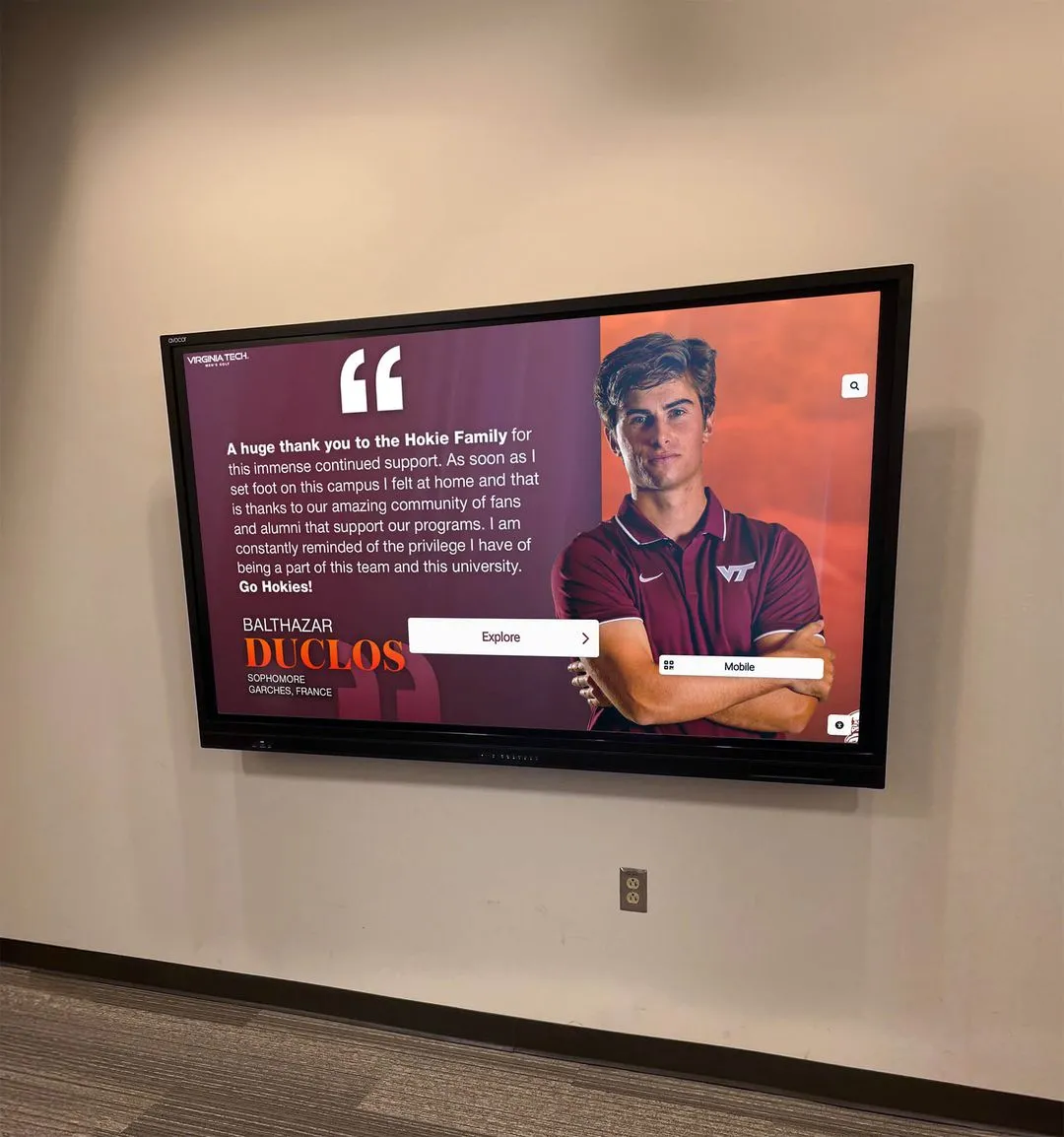

For organizations evaluating digital recognition technology as a potential use of recognition fund distributions, leading digital signage software options for school programs provide context on the range of annual technology costs the investment policy’s spending policy may need to accommodate — from basic display licensing to full content management subscriptions.

![]()

Interactive recognition kiosks create predictable annual technology costs — a recognition fund's spending policy, documented in the investment policy statement, ensures these commitments can be honored across leadership transitions without drawing on operating reserves

Review Cadence: How Often to Revisit the Policy

A booster club investment policy should be reviewed on a defined schedule. Without a scheduled review, the policy drifts out of alignment with the organization’s actual financial position as recognition programs grow, restricted gifts accumulate, or leadership priorities shift.

Annual review: The minimum standard. Conduct the review before the new season’s budget is finalized. The annual review confirms that fund categories, risk tolerance levels, and liquidity requirements still reflect the organization’s actual obligations — particularly recognition commitments that have been added, modified, or completed since the last review.

Triggered review: Any significant change in the organization’s financial position or recognition commitments should trigger an off-cycle review. Triggers include: receipt of a restricted gift above a defined dollar threshold; adoption of a new multi-year recognition technology agreement; a change in the organization’s nonprofit classification; or new guidance from the school district or state that affects nonprofit investment rules.

Officer transition review: When the treasurer changes, the incoming officer should review the investment policy within the first 60 days, confirm their understanding, and note any questions or proposed updates for board discussion at the next meeting. This prevents the common failure mode where a new treasurer operates for months without realizing a policy exists — or assumes the policy allows practices the board has actually prohibited.

The annual review cycle for the investment policy should be coordinated with the annual review of the reserve policy and the recognition obligations inventory so the three documents remain internally consistent and reflect the same understanding of the organization’s financial position and commitments.

Booster Club Investment Policy: Quick-Reference Checklist

Use this checklist to assess whether your organization’s investment policy — existing or being drafted — addresses the elements needed for sound governance.

Policy Document Elements

| Element | Requirement |

|---|---|

| Investment objectives by fund category | Stated specifically for reserves, restricted gifts, and recognition funds |

| Risk tolerance levels | Defined separately for each fund category |

| Liquidity requirements | Specified per fund category with timeline standards |

| Prohibited investments | Explicit list, approved by full board |

| Spending policy for earnings | Defined percentage or formula for recognition fund distributions |

| Commingling prevention | Account separation and accounting standards documented |

| Review schedule | Annual review date and triggered-review conditions stated |

| Board approval requirement | Policy changes require board vote documented in minutes |

Recognition Fund Governance

| Element | Requirement |

|---|---|

| Permissible expense categories | Explicit list of what recognition fund distributions may fund |

| Distribution schedule | Timing and amount of annual or periodic draws documented |

| Restricted gift accounting | Separate ledger tracking for each restricted gift with earnings attribution noted |

| Officer transition protocol | Incoming treasurer receives policy and current fund-category balances |

Frequently Asked Questions

What is a booster club investment policy?

A booster club investment policy — formally an Investment Policy Statement — is a board-approved document that defines how the organization’s financial assets are held, invested, and distributed. It covers investment objectives, risk tolerance by fund category, liquidity requirements, prohibited investments, and a spending policy for earnings. The document applies to all fund types the organization manages: general operating reserves, restricted gifts from donors or sponsors, and purpose-specific recognition funds that support awards, digital displays, or hall of fame programs.

How should a booster club handle restricted gifts from donors or sponsors?

Restricted gifts — contributions made with a condition specifying how the funds may be used — must be tracked separately from unrestricted operating reserves to prevent commingling. The investment policy should specify what account structure the organization uses to separate restricted funds, how interest or earnings on restricted balances are treated (whether they remain restricted or flow to the general fund), and what process applies if the restricted purpose cannot be fulfilled. Requirements vary by state; consult a licensed CPA or attorney for guidance on your state’s legal standards for restricted charitable funds.

Can investment earnings from a recognition fund support digital display technology costs?

Whether recognition fund earnings may support digital display technology costs depends on the fund’s governing documents and the investment policy’s defined list of permissible recognition expenses. If the fund was established to support ongoing athletic recognition programs and the board has included technology subscriptions in the permissible expense list, then annual distributions from the fund may be applied to digital display licensing, content management, and support costs. If the fund’s purpose is narrower — for example, a named award only — technology costs would need to be funded from a different source. Documenting the permissible expense categories explicitly in the investment policy prevents ambiguity across leadership transitions.

How often should a booster club review its investment policy?

A booster club investment policy should be reviewed at minimum annually, before the new season’s budget is finalized. Off-cycle reviews should be triggered by significant changes: receipt of a large restricted gift, adoption of a new multi-year recognition technology agreement, a change in the organization’s nonprofit classification, or new guidance from the school district or state. Incoming treasurers should review the policy within their first 60 days so they can manage fund categories consistently with board-approved standards from the start of their term.

Does a small booster club need a formal investment policy?

Even small booster clubs benefit from a written investment policy when they hold financial assets beyond a basic checking account — particularly when they manage restricted gifts or purpose-specific recognition funds. The policy does not need to be lengthy; a one-page document that defines fund categories, states that reserves must remain in FDIC-insured accounts, specifies that restricted gifts are tracked separately, and sets a review date provides a meaningful governance baseline. The value is not in the document’s length but in the shared understanding it creates across officers and board members, especially during leadership transitions.

Building an Investment Policy That Protects Recognition Commitments

A booster club investment policy works alongside the reserve policy and the recognition obligations inventory to form the financial governance framework that protects an athletic program’s long-term commitments. The reserve policy defines how much to hold. The recognition obligations inventory defines what commitments the reserves protect. The investment policy defines how every category of financial asset — including funds held for recognition purposes — is managed, what risk levels are appropriate, and how earnings may support the programs the organization has committed to fund.

For booster clubs that have invested in digital recognition displays, interactive hall of fame systems, or permanent athletic history installations, the investment policy creates the financial structure that sustains those commitments beyond any single fundraising cycle. A recognition fund with a documented spending policy and board-approved earnings distribution can support a digital display subscription year after year — independent of whether that year’s fundraising exceeded or fell short of expectations.

That kind of programmatic stability is what gives sponsors, donors, school administrators, and the athletes themselves confidence that the recognition commitments an organization makes will be honored not just this season but for every season the display operates, every award cycle that follows, and every officer transition that comes after.

Recognition displays that operate year over year depend on the financial governance framework the investment policy provides — a documented spending policy for recognition fund earnings ensures these displays remain funded across the leadership transitions and revenue cycles that every booster organization navigates

See What a Permanent Digital Recognition Display Looks Like for Your Program

Rocket Alumni Solutions builds interactive digital recognition displays for school athletic programs and booster clubs — giving sponsors, donors, and recognized athletes visible, lasting acknowledgment that your investment policy and recognition fund are designed to sustain. Schedule a demo to see what your program could look like.

Schedule Your Recognition Display Demo